Introduction

Many students wonder how to lower car insurance for young drivers in USA, especially when faced with staggering first-time quotes.For most young drivers in the USA, the excitement of finally holding those car keys is a major life milestone. You budget carefully for fuel, maintenance, and those monthly car payments, only to discover a harsh reality: your insurance bill quietly becomes the most expensive part of owning the vehicle.

In 2026, many students are shocked to find that their first insurance quote can sometimes cost almost as much as the car payment itself. At SwatWheelz, we believe that lowering these premiums isn’t just about finding a “cheap company”—it’s about strategically building a low-risk financial profile over time to ensure car ownership remains sustainable.

Why Car Insurance Is So Expensive for Young Drivers

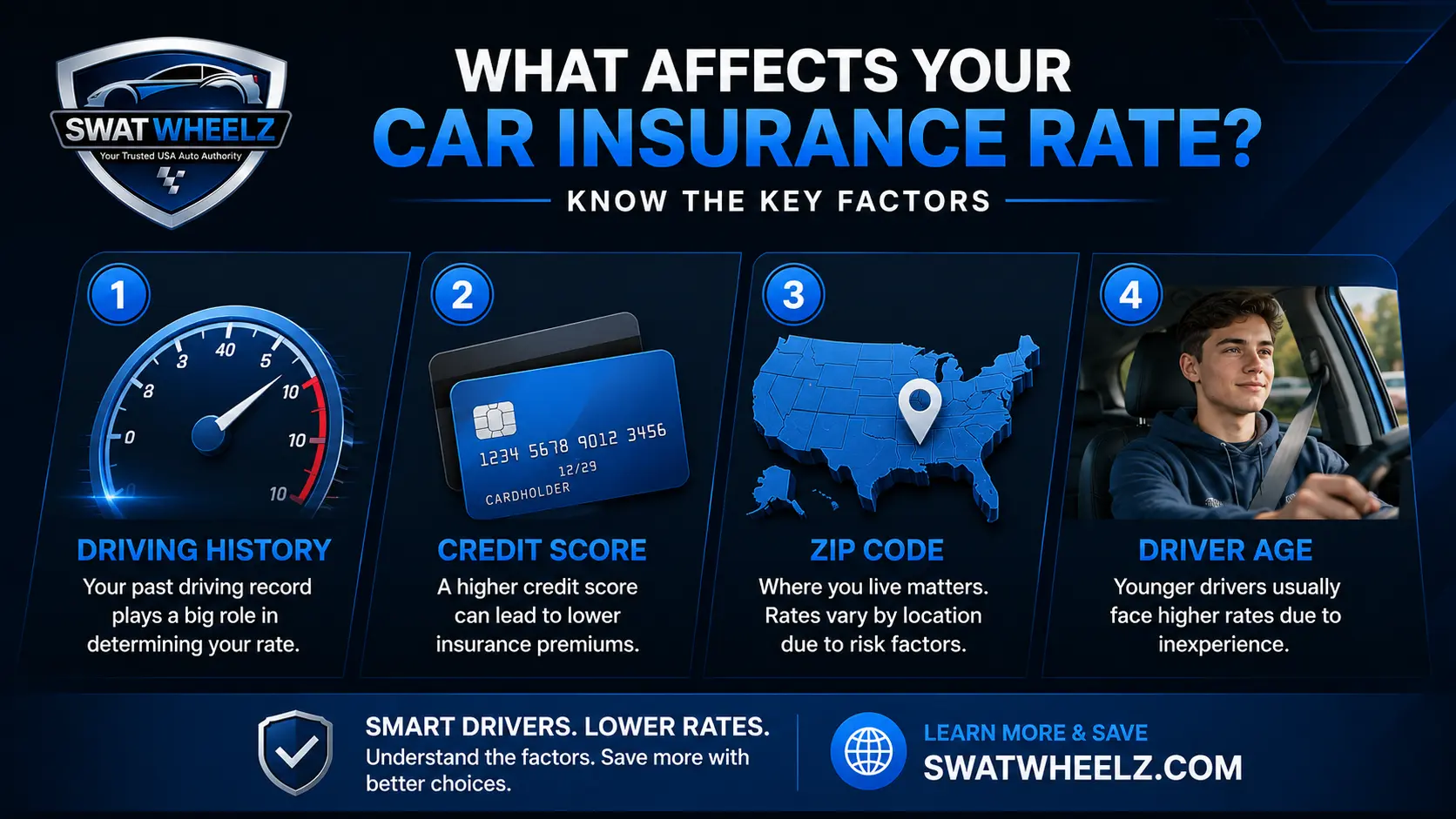

To beat the insurance companies at their own game, you first need to understand how they calculate your “Risk Profile.” Insurers aren’t just guessing; they are using decades of actuarial data to predict the likelihood of you filing a claim.

-

The Inexperience Factor: Statistics consistently show that drivers aged 16–25 have the highest rate of accidents per mile driven. Without a 10-year track record of safe driving, insurers assume the worst to protect their bottom line.

-

The Power of the Vehicle: If you’re a 19-year-old trying to insure a Mustang or a modified Dodge Charger, the “sports car risk” triggers an immediate premium hike. These cars are built for speed, and in the eyes of an insurer, speed equals expensive claims.

-

Location, Location, Location: Your ZIP code dictates your risk of theft, vandalism, and traffic density. A student in a rural Midwest town will almost always pay less than a student attending UCLA or NYU, simply because the probability of a fender-bender is lower.

-

Credit-Based Insurance Scores: Many young drivers don’t realize that in most states, your credit history (or lack thereof) is used to determine your premium. Insurers have found a correlation between financial responsibility and driving safety.

Comparison Table: Factors Impacting Your Premium

Before we dive into the solutions, let’s look at the numbers. This table represents realistic estimates of how certain factors can swing your premium in 2026.

| Factor | How It Impacts Insurance | Estimated Premium Impact | Best Way to Reduce Cost |

| Vehicle Type | Sports cars vs. Sedans | +40% to +100% | Choose a “Parking Lot King” like a Corolla. |

| Credit Score | Poor vs. Excellent Credit | +20% to +50% | Start building credit early with a student card. |

| Grades (GPA) | Under 3.0 vs. Over 3.0 | +15% to +25% | Maintain a 3.0+ GPA for the Good Student Discount. |

| Driving Record | One Speeding Ticket | +20% to +30% | Use telematics apps to prove safe habits. |

| Location | Urban vs. Rural ZIP Code | +15% to +40% | Park in a secured garage if possible. |

| Deductible | Low ($250) vs. High ($1,000) | +15% to +20% | Increase deductible if you have emergency savings. |

How Your ZIP Code Quietly Dictates Your Rates

It often feels unfair, but two identical students with the same clean driving record can pay vastly different rates just because they live on opposite sides of a city line. Insurers use your ZIP code to assess localized risk factors.

If you move from a quiet rural town to a high-density city like Philadelphia, Miami, or Los Angeles for college, expect your “Base Rate” to jump. High vehicle theft rates, frequent weather-related claims (like hail in the Midwest), and even the frequency of lawsuits in your specific area all play a role in that final number on your bill.

10 Proven Ways to Lower Car Insurance for Young Drivers

Insurance companies use complex algorithms, but you can “hack” those numbers by making smarter decisions. Here are the most effective ways to slash your premiums in 2026.

State-Specific Realities: Where Insurance Costs the Most

While your personal habits matter, your state sets the financial “floor” for your insurance. In 2026, young drivers in these states face the highest baseline costs:

-

Florida & Louisiana: High litigation rates and frequent severe weather.

-

Michigan: Unique “No-Fault” laws that require higher personal injury protection.

-

California & New York: High population density and expensive repair labor. Knowing your state’s baseline helps you understand why your initial quotes might seem so high compared to a friend living in a different part of the country.

Way #1: Stay on a Parent’s Insurance Policy

The most expensive mistake a 19-year-old can make is trying to get a standalone insurance policy. In the USA, “multi-car” and “multi-driver” discounts are massive.

-

Why it works: When you are added to your parents’ existing policy, you benefit from their long insurance history and high credit scores. Insurers view a family unit as much more stable than an individual young driver.

-

Realistic Savings: Staying on a family policy can save you anywhere from $1,000 to $2,500 per year compared to a separate individual policy.

-

Who benefits most: College students living at home or even those away at school who don’t have an established credit history yet.

Way #2: Maintain a “Good Student” GPA

Believe it or not, your report card is a financial document. Insurance companies like State Farm, GEICO, and Allstate have found a direct correlation between academic success and safe driving.

-

Why it works: Statistics show that students who are responsible enough to maintain high grades are also more responsible behind the wheel.

-

The Requirement: Most insurers require a 3.0 GPA (B average) or better. You’ll need to submit your transcript once or twice a year.

-

Realistic Savings: This single discount can knock 15% to 25% off your liability and collision premiums. For a $3,000 policy, that’s an extra $750 in your pocket.

Way #3: Choose a Cheap-to-Insure Vehicle

Before you fall in love with a car’s looks, check its “Insurance Group.” As we discussed in our Best First Cars for College Students guide, some cars are built for safety, not speed.

-

Why it works: Insurers look at “Loss Costs”—how much it costs to repair the car and how often that specific model is involved in accidents. A Honda CR-V is viewed as a safe family car; a BMW 3 Series is viewed as a high-speed risk.

-

Who benefits most: Every student. By choosing a sensible sedan or a small SUV, you avoid the “performance car tax” that insurers quietly add to your bill.

Way #4: Increase Your Deductibles Carefully

A deductible is the amount you pay out of pocket before the insurance company kicks in for a claim.

-

Why it works: By taking on more “initial risk,” you lower the insurer’s potential payout for minor fender-benders.

-

Realistic Savings: Moving from a $250 deductible to a $1,000 deductible can lower your monthly premium by 15% to 20%.

-

The Strategy: Only do this if you have $1,000 saved in an emergency fund. Don’t leave yourself stranded because you can’t afford the deductible after a minor accident.

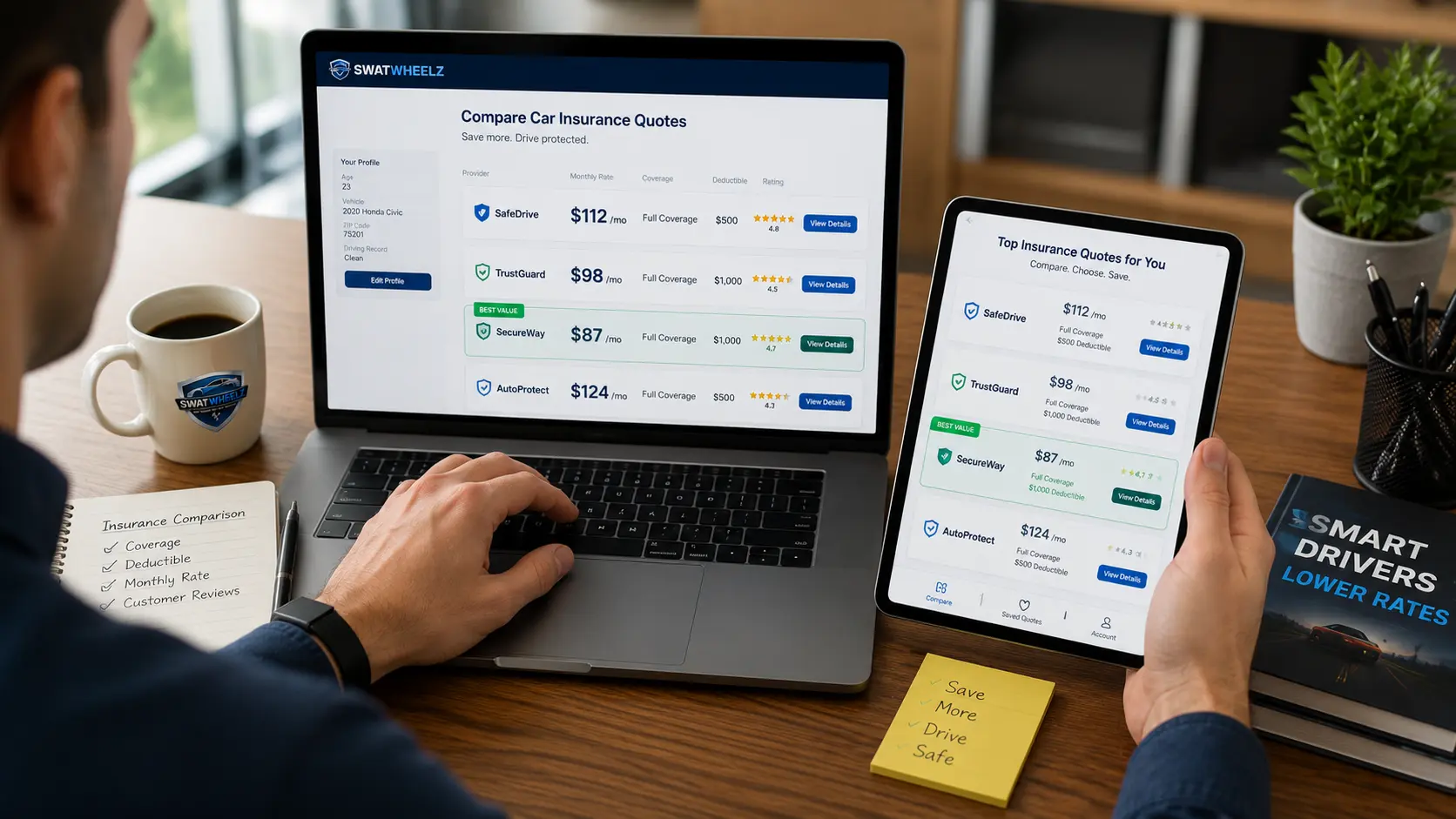

Way #5: Compare Multiple Insurance Quotes Yearly

The “Loyalty Penalty” is real. Often, insurance companies raise rates slightly every year, hoping you won’t notice.

-

Why it works: The insurance market in 2026 is highly competitive. New companies or digital-first insurers (like Lemonade or Root) might offer much better rates for your specific ZIP code than the “big names.”

-

The Strategy: Set a calendar reminder every 12 months to get at least three new quotes. It takes 30 minutes and can save you hundreds.

Way #6: Use Telematics / Safe Driving Apps

In 2026, data is more valuable than ever. Most major U.S. insurers now offer “Usage-Based Insurance” (UBI) through smartphone apps like Progressive’s Snapshot or State Farm’s Steer Clear.

-

Why it works: Instead of judging you solely on your age, the insurer judges you on how you actually drive. If the app sees that you don’t speed, brake gently, and stay off your phone, it proves you are low-risk.

-

Realistic Savings: You can earn an immediate “participation discount” just for signing up (usually 5-10%), and safe drivers can see total savings of up to 30%.

-

The Catch: If you frequently drive late at night (between midnight and 4:00 AM) or have a “lead foot,” these apps might actually show you are higher risk. Only use this if you’re a genuinely cautious driver.

Way #7: Avoid Sports Cars and “High-Theft” Models

Every young driver dreams of a Mustang or a BMW, but in the insurance world, these are “Red Flag” vehicles.

-

Why it works: The reason insurers offer this is simple…” ya “From an insurer’s perspective..

-

The Math: Insuring a sports car”: > In reality, for many young drivers, switching from a Mustang or a high-performance Dodge to a sensible Toyota Corolla can literally cut insurance costs in half overnight.

-

Reference: Check our guide on Best First Cars for College Students for models that insurers actually love.

Way #8: Bundle Auto + Renters Insurance

Most college students rent an apartment or a dorm room. Even if you don’t own much, getting a “Renters Insurance” policy can actually save you money on your car.

-

Why it works: This is called “Bundling.” Insurance companies want as much of your business as possible. When you have two policies with the same company, they give you a Multi-Policy Discount.

-

The Reality: A Renters policy might cost you $15 a month, but the discount it triggers on your $200 car insurance could be $30. You’re essentially getting protected for free and saving money.

Way #9: Improve Your Credit Score

This is the “Hidden Factor” ChatGPT mentioned. In 2026, in almost every U.S. state (except California, Hawaii, and Massachusetts), insurers use your Credit-Based Insurance Score to set your rates.

-

Why it works: Data shows that people who manage their finances responsibly (paying bills on time, low credit card debt) tend to be more responsible drivers.

-

The Impact: A young driver with a “Good” credit score (700+) can pay 20% to 40% less than someone with “Poor” or no credit.

-

Action Step: Get a student credit card early, keep the balance low, and never miss a payment. It’s one of the best long-term insurance strategies.

Way #10: Take a Certified Defensive Driving Course

In many states, completing a voluntary, state-approved safety course can trigger a mandatory discount on your premium.

-

Why it works: It proves to the insurer that you are proactive about safety and understand the rules of the road better than the average teen.

-

Realistic Savings: Usually a 5% to 10% discount for three years.

-

The Bonus: These courses (often available online for $25-$50) can also help remove “points” from your license if you’ve already had a minor ticket, preventing your rates from skyrocketing further.

Cheapest Types of Cars to Insure for Young Drivers

The logic used by insurance companies is simple: the more expensive a car is to repair or the faster it goes, the higher the premium. If you want to save on insurance, you should choose what are known as “Insurers’ Favorites.”

-

The Winners (Cheapest to Insure):

-

Toyota Corolla & Camry: Known for low repair costs and solid safety features.

-

Honda CR-V: SUVs are often cheaper to insure than sedans because they are categorized as “family vehicles.”

-

Subaru Outback: These vehicles have exceptionally high crash-test ratings, which insurers love.

-

Mazda3: Offers a perfect balance of style and insurance affordability.

-

-

The Losers (Most Expensive to Insure):

-

Muscle Cars (Mustang, Camaro, Charger): These have the highest accident rates among young drivers.

-

Luxury German Cars (BMW 3 Series, Audi A4): Even a simple side-mirror replacement can cost thousands, leading to sky-high premiums.

-

Modified Cars: Any after-market modifications can lead an insurer to label the vehicle as “high-risk.”

-

Choosing the right model is half the battle. Students looking for insurance-friendly vehicles should also explore our Best First Cars for College Students guide to see which models offer the best safety-to-premium ratio.

Hidden Insurance Discounts Most Students Ignore

Saving money requires looking beyond just the Good Student Discount. In 2026, here are several additional discounts you can claim:

-

Distant Student Discount: If you are away at college and your car stays at your parents’ home (usually more than 100 miles away), your premium can drop by up to 20% because you aren’t driving the car daily.

-

Low-Mileage Discount: If you drive less than 7,500 miles a year, let your insurer know. Less time on the road means less risk of an accident.

-

Paperless & Auto-Pay Discounts: Simply opting for digital billing and setting up automatic payments can save you $50–$100 annually.

-

Military Family Discounts: If your parents or siblings are in the U.S. Military, insurers like USAA or GEICO offer significant specialized discounts.

Full Coverage vs. Liability: Which One Do You Need?

Young drivers often make the mistake of choosing “minimum coverage” to save money, but sometimes paying for full coverage is the smarter financial move.

-

Liability Only: This only covers damages to the other party. If your car is an older model worth less than $5,000, this is usually the best choice as paying high premiums for a low-value car doesn’t make sense.

-

Full Coverage (Comprehensive + Collision): If you have a car loan or lease, this is mandatory. It covers damage to your own vehicle regardless of who is at fault, as well as theft and weather damage.

To put this into perspective, a financed 2024 Honda Civic with full coverage (including collision and comprehensive) might cost around $220/month to insure for a student. On the other hand, an older, paid-off Corolla with liability-only coverage could cost under $95/month. The key is balancing the value of your car against the protection you actually need.

The key is balancing the value of your car against the protection you actually need. While liability limits protect others, don’t ignore uninsured motorist coverage, especially in states like Florida where many drivers lack insurance. These comprehensive claims can save you from financial ruin if your car is damaged by someone else’s mistake.

The Massive Impact of Credit Scores on Insurance

In the USA, your driving record is only one part of the puzzle; your financial history, specifically your credit score, plays a massive role in determining your premium. Many young drivers are unaware that their “Credit-Based Insurance Score” can increase or decrease their monthly bill by as much as 50%.

-

Financial Responsibility = Driving Safety: Insurance companies use actuarial data suggesting that individuals who manage their finances responsibly—paying bills on time and maintaining low debt—are statistically less likely to be involved in accidents.

-

The Premium Difference: A young driver with a credit score of 750+ can save thousands of dollars compared to a peer with a score below 600, even if both have perfectly clean driving records.

-

2026 Strategy: If you haven’t built a credit history yet, consider using “Credit Builder” apps or a student-specific credit card. Most insurance companies review your score every six months, so your rates could drop as soon as your credit improves.

Common Insurance Mistakes Young Drivers Make

To provide the best advice for our readers, we must highlight the common pitfalls that can devastate a student’s budget:

-

Buying the “Cool” Car Too Early: Choosing a sports car or a modified vehicle during your college years is a major financial mistake due to the massive insurance surcharges.

-

Allowing Coverage Lapses: Even a one-week gap in insurance coverage can cause insurers to label you as “High Risk,” leading to significantly higher premiums when you try to restart a policy.

-

Hiding Drivers from Your Policy: Failing to list a roommate or frequent driver on your policy can be considered “Insurance Fraud,” which may lead to your claims being denied in the event of an accident.

-

Choosing Low Deductibles Without Savings: A $100 deductible sounds attractive, but it can add $50 or more to your monthly premium. Only choose a low deductible if you cannot afford a higher out-of-pocket cost during an emergency.

Real-Life Example: The Tale of Two Drivers

Let’s look at how strategic choices impact the bottom line. Here are realistic 2026 USA insurance rate comparisons:

Driver A (The Expensive Way):

-

Age: 19 years old

-

Vehicle: Used Ford Mustang (Sports Car)

-

Policy Type: Individual (Standalone)

-

GPA: 2.5 (No Good Student Discount)

-

Monthly Premium: $420

-

Yearly Cost: $5,040

Driver B (The SwatWheelz Way):

-

Age: 20 years old

-

Vehicle: Toyota Corolla (Sedan)

-

Policy Type: Family Policy (Added to parents)

-

GPA: 3.6 (Good Student Discount applied)

-

Telematics App: Enabled (Safe Driver Discount applied)

-

Monthly Premium: $165

-

Yearly Cost: $1,980

Total Yearly Savings for Driver B: $3,060! This $3,060 can cover an entire year’s worth of textbooks, fuel, or campus housing for a proactive student.

Choosing Your Partner: Traditional vs. App-Based Companies

In 2026, you aren’t limited to the old-school names. You generally have two paths:

-

The Legacy Giants (GEICO, State Farm, Progressive): Best for stability and bundling with a parent’s policy.

-

Digital Disrupters (Root, Lemonade, Metromile): These are app-based companies that rely heavily on telematics. If you are a cautious student who doesn’t drive many miles, their “pay-per-mile” or behavior-based models can often be 20% cheaper than traditional quotes.

Step-by-Step Guide to Finding Affordable Insurance

If you are looking for insurance for the first time, do not simply take the first quote you receive. Follow this systematic process to ensure you get the best deal:

-

Gather Your Information: Have your Driver’s License number, Vehicle Identification Number (VIN), and school transcript (for GPA verification) ready before starting.

-

Compare at Least 3 Quotes: Use online comparison tools like The Zebra or Insurify, or visit the websites of major providers like GEICO, Progressive, and State Farm directly to request quotes.

-

Check Your Deductibles: When requesting a quote, compare the difference in premiums between a $500 vs. $1,000 deductible. This can significantly change your monthly cost.

-

Review Coverage Limits: While every state in the USA has its own “Minimum Liability” requirements, it is often better to carry slightly higher coverage to protect your assets and your vehicle.

-

Ask for “Unlisted” Discounts: Speak with an agent directly and ask: “Do you offer any specialized discounts for distant students or for completing defensive driving courses?”

Frequently Asked Questions (FAQs)

Q1: Does my credit score really affect my insurance as a student? A: Yes, significantly. In almost every U.S. state, insurers use a “Credit-Based Insurance Score.” They’ve found a statistical link between how people manage their finances and how they drive. Even if you don’t have a long history, starting a student credit card and paying it on time can lower your long-term insurance costs by 20% or more.

Q2: Is full coverage actually worth the extra cost for young drivers? A: This depends entirely on the value of your vehicle. If you are driving a car worth more than $5,000 or if you have an active car loan, Collision and Comprehensive coverage are essential. However, if your car is an older “beater” worth very little, paying for full coverage might cost you more in premiums over two years than the car is actually worth.

Q3: Why does my ZIP code matter if I’m a safe driver? A: Because insurance is a pool of risk. If you live in an area with high rates of uninsured motorists or frequent car thefts, the insurance company assumes a higher probability that they will have to pay out a claim for your car, even if you never cause an accident yourself.

Q4: Can I stay on my parents’ insurance if I live away at college? A: Yes, and this is often the most strategic move. As long as your permanent address is still your parents’ home, most U.S. insurers allow you to stay on the family policy. This lets you benefit from their long-term insurance history and multi-car discounts, which is significantly cheaper than starting your own standalone policy.

Q5: Does a single speeding ticket really increase my rates that much? A: Unfortunately, yes. For a young driver, one speeding ticket can trigger a 20% to 30% hike in premiums. Insurers view tickets as a sign of high-risk behavior. However, taking a defensive driving course can sometimes help mitigate this increase or even remove the points from your license entirely.

Q6: Are telematics and safe-driving apps actually private? A: Most insurance apps track your location, speed, and braking habits. While they use this data strictly to calculate your discount, you should always read the privacy policy. For most students, the trade-off—a 30% discount—is worth the data sharing, as long as you are a cautious driver.

Q7: Why does my gender affect my car insurance rates in the USA? A: Statistics show that young male drivers are involved in more high-speed accidents than young female drivers. While some states like California and Hawaii have banned gender-based pricing, in most other states, young men will naturally see slightly higher initial quotes.

Q8: How often should I shop around for new insurance quotes? A: You should compare quotes at least once every 12 months. Insurance companies frequently update their risk algorithms for specific ZIP codes. A company that was expensive for you last year might be the most affordable this year, especially as you gain more months of clean driving experience.

Q9: What is the ‘Distant Student Discount’ and do I qualify? A: If you attend a college that is more than 100 miles away from home and leave your car at your parents’ house, you likely qualify. Insurers offer this because the car is sitting safely in a driveway rather than being driven in busy campus traffic, leading to substantial premium drops.

Q10: Is it better to choose a high or low deductible? A: A high deductible (like $1,000) lowers your monthly bill but requires you to have that cash ready in case of an accident. A low deductible ($250) is more convenient during a claim but makes your monthly premium much higher. For most students, a $500 deductible provides a balanced middle ground.

Conclusion

For most students, the cheapest insurance policy is rarely the smartest long-term choice. The real goal is building a safe driving history, maintaining affordable coverage, and avoiding financial surprises during college. At SwatWheelz, we believe that treating your insurance as a long-term financial asset—rather than just another monthly bill—is the key to automotive freedom in 2026.