Introduction

Finding the cheapest car insurance for young drivers in USA is more challenging than ever in 2026. Rising repair costs, inflation, and advanced vehicle technology have pushed premiums to record highs — especially for drivers under 25.The financial burden is even more significant. Statistics from early 2026 show that the average full-coverage premium for a driver under 20 is now exceeding $6,000 annually in many states.According to a recent 2026 analysis by Forbes Advisor

However, “expensive” does not have to be the final word. Navigating the maze of quotes, policy terms, and state-specific mandates requires a strategic approach. Whether you are a college student in New York or a young professional starting a career in Texas, finding the right balance between cost and coverage is essential. This comprehensive guide provides a deep dive into the 2026 insurance landscape, identifying the cheapest carriers and the most effective ways to slash your premiums.

The 2026 State of the Insurance Market

Before choosing a provider, it is crucial to understand why rates vary so drastically across the United States. In 2026, several factors are influencing the quotes you see online:

-

EV and Tech Integration: Repairing a modern car’s sensors and battery packs is more expensive than traditional mechanical fixes.

-

Inflationary Pressure: Parts and labor costs have risen, leading insurance companies to adjust their risk models.

-

Regional Risk Profiles: Florida and Louisiana remain the most expensive states due to high litigation costs and weather-related risks, while states like Vermont and Ohio continue to offer more affordable rates.

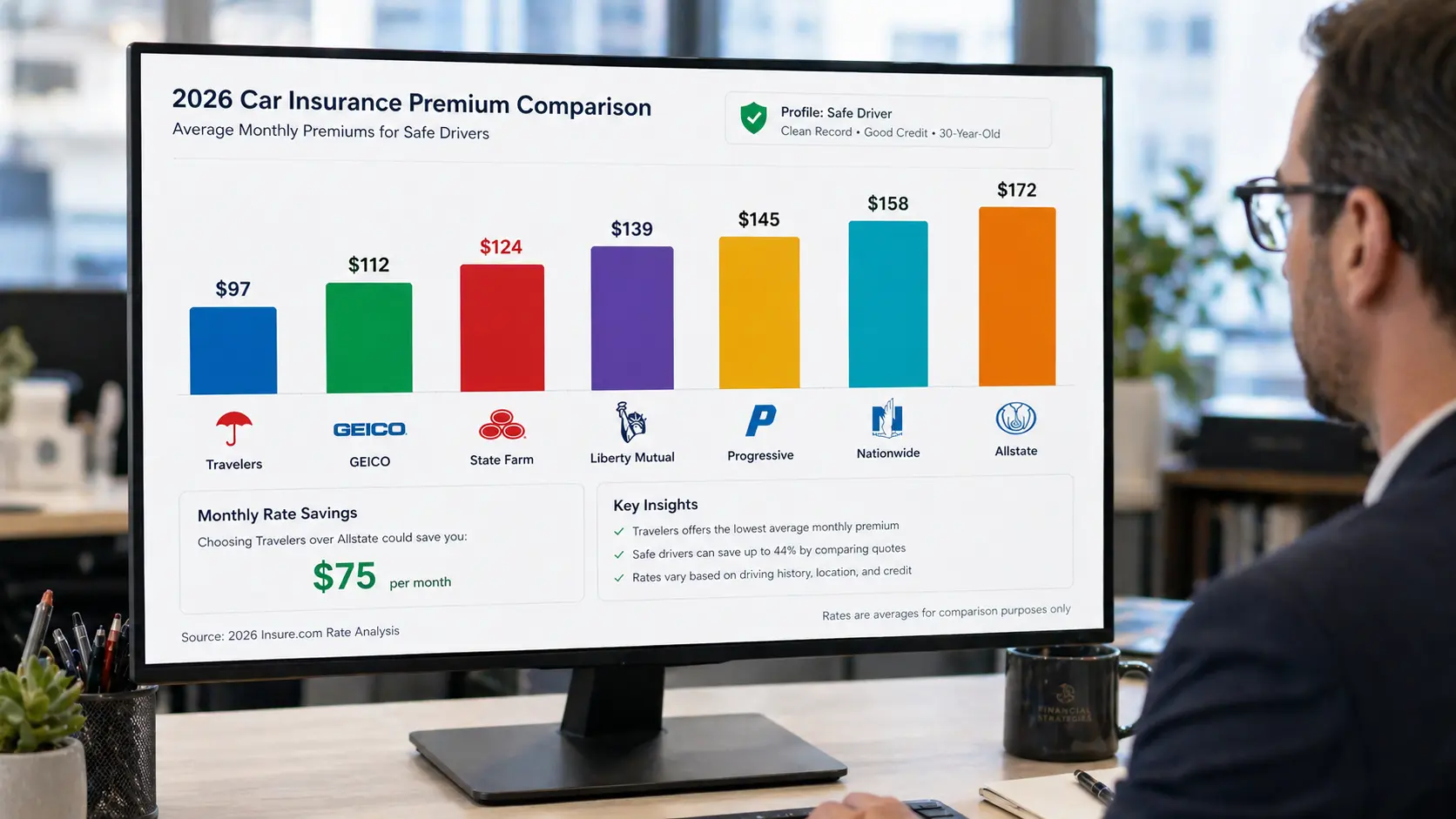

Comprehensive 2026 Market Comparison Table

For a quick overview of the most competitive players this year, refer to the table below. These figures are based on national averages for a 21-year-old driver with a clean record and a mid-sized sedan.

Here’s a quick comparison of the cheapest car insurance providers for young drivers in 2026:

| Insurance Provider | Best Category for 2026 | Avg. Monthly Rate | Unique Discount |

|---|---|---|---|

| Travelers | Cheapest Overall | $139 | IntelliDrive® |

| GEICO | Digital Service | $155 | DriveEasy |

| State Farm | Best for Students | $177 | Steer Clear® |

| Nationwide | Flexible Coverage | $165 | SmartRide® |

| Progressive | High-Risk Drivers | $182 | Snapshot® |

| Erie | Regional Choice | $175 | Rate Lock™ |

| USAA | Military Families | $128 | Family Rates |

In-Depth Analysis: The Top 3 Budget-Friendly Carriers

1. Travelers: The Value Leader of 2026

Travelers has solidified its position as the go-to carrier for cost-conscious young adults in 2026. Their premiums are consistently 10–15% lower than the national average.

-

The IntelliDrive Advantage: This is a 90-day telematics program via a smartphone app. In 2026, the software has become highly accurate at rewarding safe driving habits—such as gentle braking and avoiding late-night driving—with discounts up to 30%.

-

Who it’s for: Best for disciplined drivers who don’t mind their habits being monitored for a few months to lock in a permanent lower rate.

2. GEICO: The Digital Native’s Choice

GEICO remains a dominant force due to its low overhead costs and massive national footprint. In 2026, their mobile app is considered the benchmark for filing claims and managing policies.

-

Good Student Discount: GEICO has doubled down on academic rewards. Full-time students with a “B” average or higher can see significant reductions.

-

Multi-Policy Power: Bundling your car insurance with a renters policy (even if you’re in a dorm) can trigger a “Multi-Policy” discount that often pays for the renters insurance itself.

3. State Farm: The Community Favorite

State Farm is unique because it combines a national reach with the “human touch” of local agents. In 2026, they are particularly focused on the 18–25 demographic through education.

-

Steer Clear® Program: This is more than just an app; it’s a certification course. By completing safe driving modules and logging driving hours, young drivers prove their reliability to the insurer.

-

Broadest Network: For drivers who want a personal agent in their local neighborhood to explain their policy, State Farm is the primary choice.

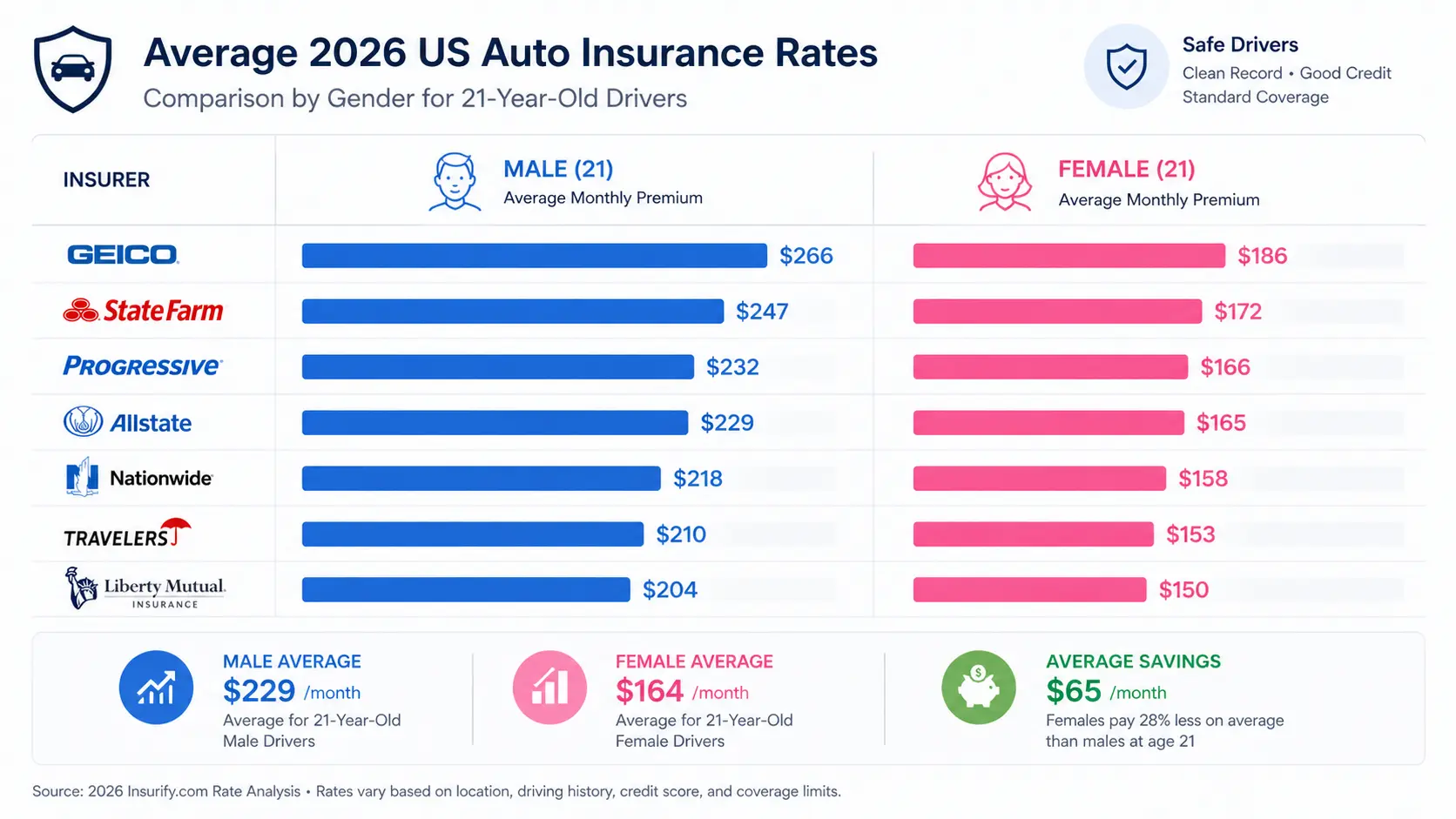

Gender and Age: The 2026 Price Gap Explained

-

One of the most controversial yet impactful factors in US car insurance is how age and gender interact. As of April 2026, the data shows a staggering difference in premiums for the youngest drivers. For instance, a 16-year-old male driver in 2026 pays an average of $10,928 annually, while a female of the same age pays $9,846. This gap narrows as drivers reach age 25, eventually stabilizing by age 30 where the difference is less than $10.

However, it is vital for readers to know that not all states allow this. If you are in California, Hawaii, Massachusetts, Michigan, or North Carolina, state laws prohibit insurers from using gender as a rating factor. Knowing these local regulations can help you identify if you are being overcharged.

-

Pros and Cons of the “Big Five” Insurers

To help you make an informed decision, here is a balanced look at the major players in the 2026 market:

Travelers

-

Pros: Consistently the lowest rates for those who drive safely; unique “Rate Lock” options in some states.

-

Cons: Their digital interface, while functional, lacks the high-end polish of competitors like GEICO.

GEICO

-

Pros: Best-in-class mobile app; massive discounts for government employees and military.cheapest car insurance for young drivers USA

-

Cons: Rates tend to increase sharply if you have even one minor “at-fault” fender bender.

Progressive

-

Pros: “Name Your Price” tool is perfect for budget-conscious Gen Z; very lenient with drivers who have a “thin” credit history.

-

Cons: The Snapshot® telematics program can actually increase your rates if it detects aggressive driving.

State Farm

-

Pros: The “Steer Clear” program is the best educational tool for teens; local agents provide personalized service.

-

Cons: Premiums are often slightly higher than GEICO or Travelers for those with perfect records.

Nationwide

-

Pros: Their SmartRide® program offers a guaranteed discount just for signing up; great for low-mileage drivers.

-

Cons: Not always the cheapest option for high-mileage daily commuters.

The “Parental Policy” Strategy: Is it Always Cheaper?

-

-

In 2026, adding a teen or young adult to a parent’s policy remains the most common way to save. On average, a standalone policy for an 18-year-old costs $6,779, but adding them to a multi-car family policy can bring that down to $5,113. That is a $1,666 annual saving.

-

Tip: If the student is moving away for college (more than 100 miles) and leaving the car at home, ask for the “Student Away at School” discount. This can slash the premium by up to 30% because the risk of an accident is significantly lower.

Step-by-Step Guide: How to Negotiate Your 2026 Premium

-

Audit Your Annual Mileage: With more remote work and hybrid classes in 2026, many young drivers are overestimating their miles. If you drive less than 7,500 miles a year, you qualify for a “Low Mileage” tier.cheapest car insurance for young drivers USA

-

The “Deductible Math”: Moving your deductible from $500 to $1,000 typically saves 15-30% on the collision portion of your premium. If you have $1,000 in emergency savings, this is a “no-brainer” move. Bankrate’s guide on reducing auto insurance premiums

-

Check Your Credit-Based Insurance Score: In states where it’s legal, your credit score is as important as your driving record. A “Good” credit score can save you up to $200 annually compared to a “Poor” score.

-

Completion of Defensive Driving: Taking a 6-hour online course approved by your state’s DMV can yield a mandatory 5-10% discount for three consecutive years.

Real-World Scenario: The “First Car” Choice

-

-

Consider two 21-year-old friends in Florida.

-

Friend A buys a 2026 Ford Mustang (Sports Car). His premium: $919/month.

-

Friend B buys a 2026 Honda CR-V (SUV). His premium: $220/month. The choice of vehicle is the single biggest factor you can control besides your driving record.

State-Specific Insights: Finding Gold in Local Regulations

In 2026, the state you live in is the biggest “hidden” factor in your insurance cost. Every US state has different minimum liability requirements. Let’s look at two key states where young drivers often struggle:

-

New York (The High-Risk Hub): If you are driving in NYC or surrounding boroughs, you are required to have “No-Fault” insurance (Personal Injury Protection). Because New York is a “no-fault” state, your rates will naturally be 20-30% higher than the national average. Pro Tip: Look for regional carriers like NYCM Insurance or Plymouth Rock for localized discounts that national giants like GEICO might miss.

-

Texas (The Competitive Frontier): Texas has a massive market with over 200 insurance providers. While the state average is moderate, “Uninsured Motorist Coverage” is essential here, as nearly 14% of drivers in Texas remain uninsured in 2026.

The 2026 Tech Trend: Why Dash Cams are Your Best Friend

-

-

While most insurance companies don’t give a direct discount for having a dash cam yet, they are becoming essential for young drivers. In 2026, many “at-fault” disputes are settled instantly using 4K dash cam footage. For a young driver, proving you were not at fault in a collision can save you from a 40% premium hike that would otherwise last for three years.

Comprehensive FAQ Section (Addressing User Intent)

1. What is the absolute cheapest car for a 16-year-old to insure in 2026?

-

Statistically, older mid-sized SUVs like the Honda CR-V or Subaru Outback are the cheapest. Avoid luxury brands or high-horsepower sports cars, as they carry the highest “risk multipliers.”

-

2. Does “Usage-Based Insurance” (UBI) really save money?

-

Yes. In 2026, safe drivers using UBI programs like Allstate’s Drivewise or State Farm’s Steer Clear save an average of $450 per year. However, if you often drive late at night or exceed speed limits, these programs might not be for you.

- cheapest car insurance for young drivers USA

-

3. Can I get insurance with a foreign driving license in the USA?

-

Yes, companies like Progressive and State Farm often accept international licenses, but you will likely be charged a “New Driver” rate until you obtain a US state license.

4. How long do accidents stay on my record in 2026?

-

Most US insurers look back 3 to 5 years. If you had an accident in 2023, it should begin to fall off your record by late 2026, leading to a significant rate drop.

5. Is “Liability Only” insurance illegal?

-

No, it is legal as long as you meet your state’s minimum requirements. However, if you have a car loan, your lender will require you to have full coverage (Collision and Comprehensive).

6. What happens if I drive without insurance in 2026?

-

The penalties have become stricter. You could face heavy fines (up to $1,500), license suspension, and in states like California, your vehicle could be impounded on the spot.

7. Does getting a ticket for “Texting and Driving” affect my rates?

-

In 2026, distracted driving is treated almost as severely as a DUI by some insurers. Expect a 15–25% increase in your premium after one conviction.

8. Can I change my insurance company at any time?

-

Yes. You do not have to wait for your policy to expire. If you find a cheaper rate mid-month, you can switch and get a pro-rated refund from your old company.

9. Are there discounts for electric vehicles (EVs) in 2026?

-

While some companies offer “Green Vehicle” discounts, the high cost of EV repairs often cancels this out, making EVs slightly more expensive to insure than hybrids.

10. How does a gap in insurance coverage affect my future rates?

-

A coverage gap of even 30 days makes you a “High Risk” driver in the eyes of an algorithm. Always maintain continuous coverage to keep your “Loyalty” and “Continuous Coverage” discounts active.

Final Verdict: The SwatWheelz Recommendation

Navigating 2026 car insurance as a young driver requires a mix of technology, research, and smart vehicle choices. If you want the absolute lowest price and are a safe driver, Travelers with IntelliDrive is your winner. If you are a student looking for long-term stability and educational discounts, State Farm is the superior choice.

Don’t let the high premiums of 2026 stop you from getting on the road. Audit your policy every six months, keep your GPA high, and always compare at least three quotes before signing.

-